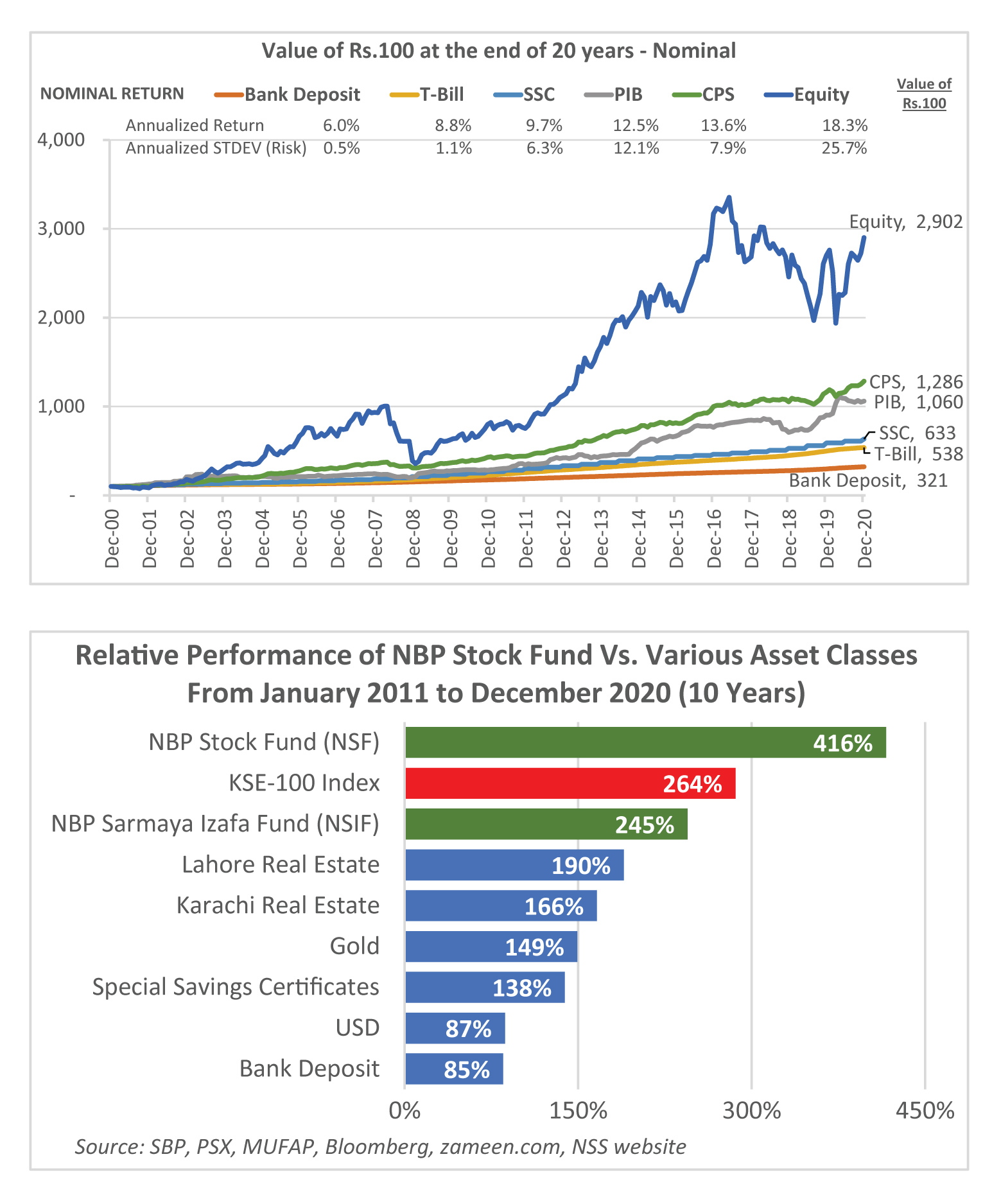

The last four years have been challenging for the stock market. This subdued performance of the stock market has come after eight years of robust returns during which the KSE-100 Index surged by around 807%. Looking at the long-term performance of the stock market, it is evident that these depressed periods do not stay forever. In the long run, equity has outperformed all the other asset classes, although it is volatile in the short-term. Historical market data cannot predict the future but it is still a useful guide to understand the potential risks and rewards for investors. With that in mind, we examine past performance of key domestic asset classes for a 20-year period from January 2001 to December 2020. We have included six asset categories for which long-term data is available: Treasury Bills, Bank Deposits, National Savings Schemes (NSS), Pakistan Investment Bonds (PIBs), Capital Protected Strategy (CPS), and Equities. CPS is a synthetic asset class under which portfolio is dynamically managed between the low risk and high risk components with the aim of capital preservation, while also capturing some upside of the stock market. The results of the CPS are based on back-testing as this strategy was not in practice during this entire period. Inflation as measured by CPI has averaged 7.9% per annum, and Pak Rupee has depreciated against the US Dollar by 5.2% per year, over the last twenty years.

The historical analysis, as given in the Table below depicts that equities offered the highest nominal and real return amongst all the asset classes. An investment of PKR 100 in equities in January 2001 would be worth PKR 2,902 by the end of December 2020. During the same period, PKR 100 investment in bank deposits or T-Bills would have increased to a paltry PKR 321 and PKR 538, respectively.

The outcome of the above analysis supports the basic notion that there is a positive relationship between risk and return, meaning higher the risk the higher the return. In line with the expectation, equities exhibited the highest volatility, and bank deposits and T-Bills have the lowest risk. The analysis also shows that over a long investment horizon, equities delivered the highest return.

One take away from this analysis is that investors with long-term goals like educating their children, owning a house, or saving for their retirement should have some of their assets invested in equities, preferably through equity mutual funds, while investors with low-risk appetite due to short term investment needs, should invest in bank deposit or as an alternative in money market / income funds.

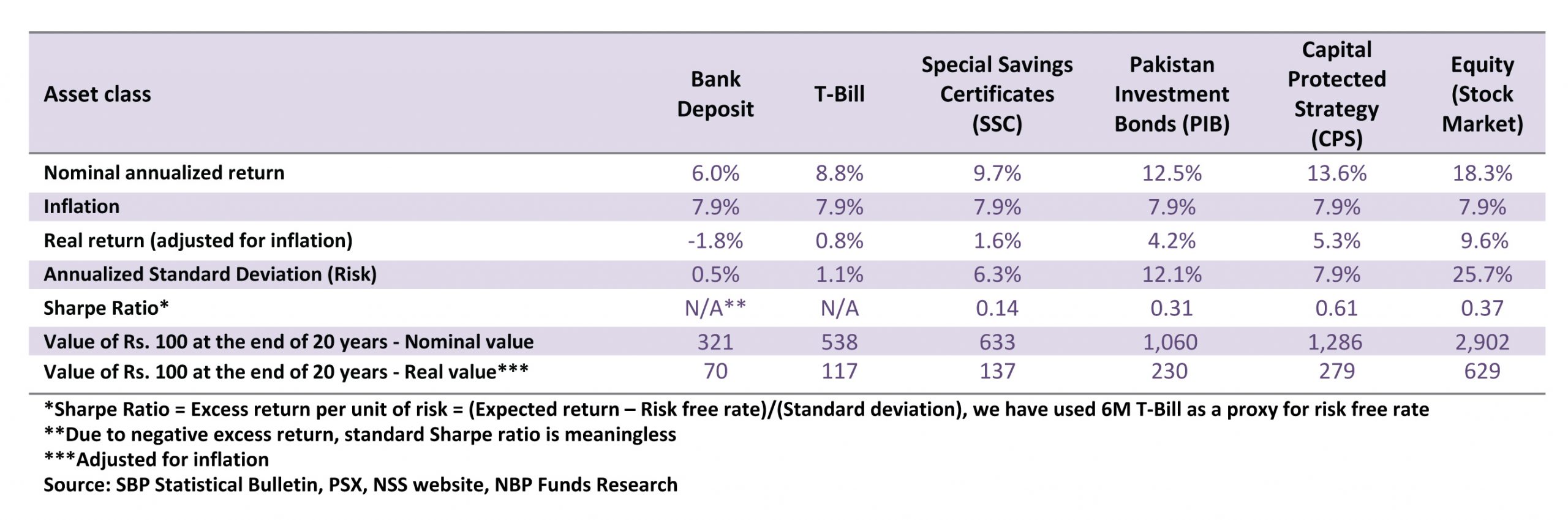

Well managed equity mutual funds have provided better returns to their investors than the stock market and other asset classes including real estate over the last ten (10) year period. For performance comparison, we have used the index provided by zameen.com for the performance of real estate sector. As a case in point, our flagship equity fund, NBP Stock Fund (NSF) has out-performed the stock market by 152% over the last 10 years (from January 2011 till December 2020) by earning a return of 416% versus 264% rise in the stock market. An investment of Rs. 100 in NBP Stock Fund 10 years ago would have grown to Rs. 516 today, whereas an investment of Rs. 100 in the stock market (KSE-100 Index) 10 years ago would be worth Rs. 364 today. This out-performance of the Fund is net of management fee, and all other expenses.